All Categories

Featured

[/image][=video]

[/video]

Withdrawals from the money value of an IUL are generally tax-free approximately the amount of costs paid. Any kind of withdrawals above this amount may undergo taxes relying on plan structure. Typical 401(k) payments are made with pre-tax dollars, reducing gross income in the year of the payment. Roth 401(k) contributions (a plan feature available in many 401(k) strategies) are made with after-tax payments and afterwards can be accessed (profits and all) tax-free in retired life.

Withdrawals from a Roth 401(k) are tax-free if the account has actually been open for at least 5 years and the person mores than 59. Assets withdrawn from a standard or Roth 401(k) before age 59 may sustain a 10% charge. Not exactly The cases that IULs can be your own bank are an oversimplification and can be deceiving for many factors.

You may be subject to upgrading connected health questions that can impact your ongoing prices. With a 401(k), the cash is constantly yours, consisting of vested company matching regardless of whether you quit adding. Threat and Guarantees: Most importantly, IUL plans, and the cash money value, are not FDIC insured like basic financial institution accounts.

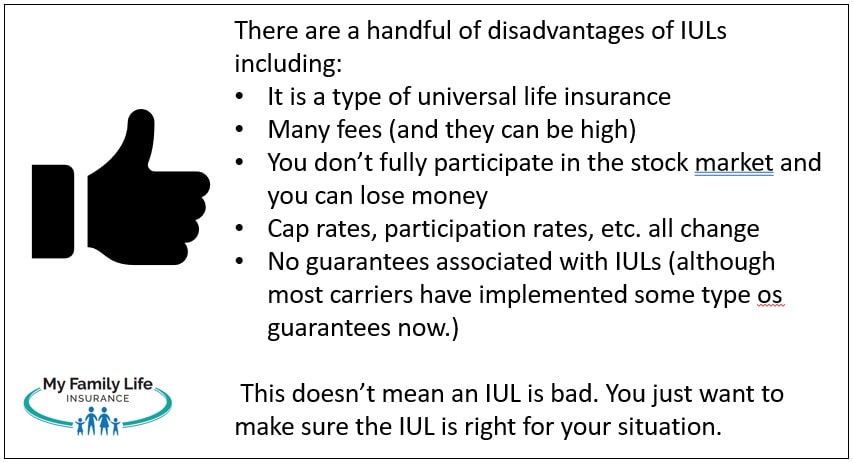

While there is generally a floor to avoid losses, the growth potential is capped (suggesting you may not completely gain from market growths). The majority of professionals will concur that these are not equivalent items. If you desire death advantages for your survivor and are worried your retired life savings will certainly not suffice, after that you may want to think about an IUL or other life insurance coverage item.

Sure, the IUL can supply access to a cash money account, yet once more this is not the primary function of the product. Whether you want or need an IUL is a highly private inquiry and relies on your main financial objective and objectives. However, below we will attempt to cover advantages and constraints for an IUL and a 401(k), so you can further mark these products and make a more enlightened decision regarding the finest means to handle retirement and taking care of your liked ones after death.

Maximum Funded Indexed Universal Life

Loan Costs: Lendings versus the plan accumulate rate of interest and, if not paid back, decrease the survivor benefit that is paid to the beneficiary. Market Involvement Restrictions: For the majority of plans, financial investment growth is linked to a securities market index, but gains are normally covered, restricting upside prospective - iul insurance pros and cons. Sales Practices: These policies are frequently marketed by insurance policy agents that might highlight advantages without totally discussing costs and risks

While some social networks experts suggest an IUL is a replacement product for a 401(k), it is not. These are various items with different goals, attributes, and costs. Indexed Universal Life (IUL) is a type of long-term life insurance coverage policy that likewise uses a money value part. The money worth can be made use of for multiple functions consisting of retired life savings, extra revenue, and other economic demands.

%20Insurance%20Policy%20-%20Amplify%0A%0A){kind=link}

Latest Posts

Transamerica Financial Foundation Iul Reviews

E Learning Iscte Iul Pt

Iul For